The banking complaints conundrum: Are UK banks losing the trust battle?

Thought Leadership

As originally published by The Payments Association.

The latest complaints data from the Financial Conduct Authority (FCA) offers a critical window into the state of customer trust across the UK financial services industry. While the headline figures might suggest a market-wide improvement, a deeper look reveals a more complex and challenging reality for the banking and credit card sector.

The patterns emerging from the second half of 2024 complaints data suggest that banks face a fundamental challenge in maintaining customer trust during their most vulnerable moments.

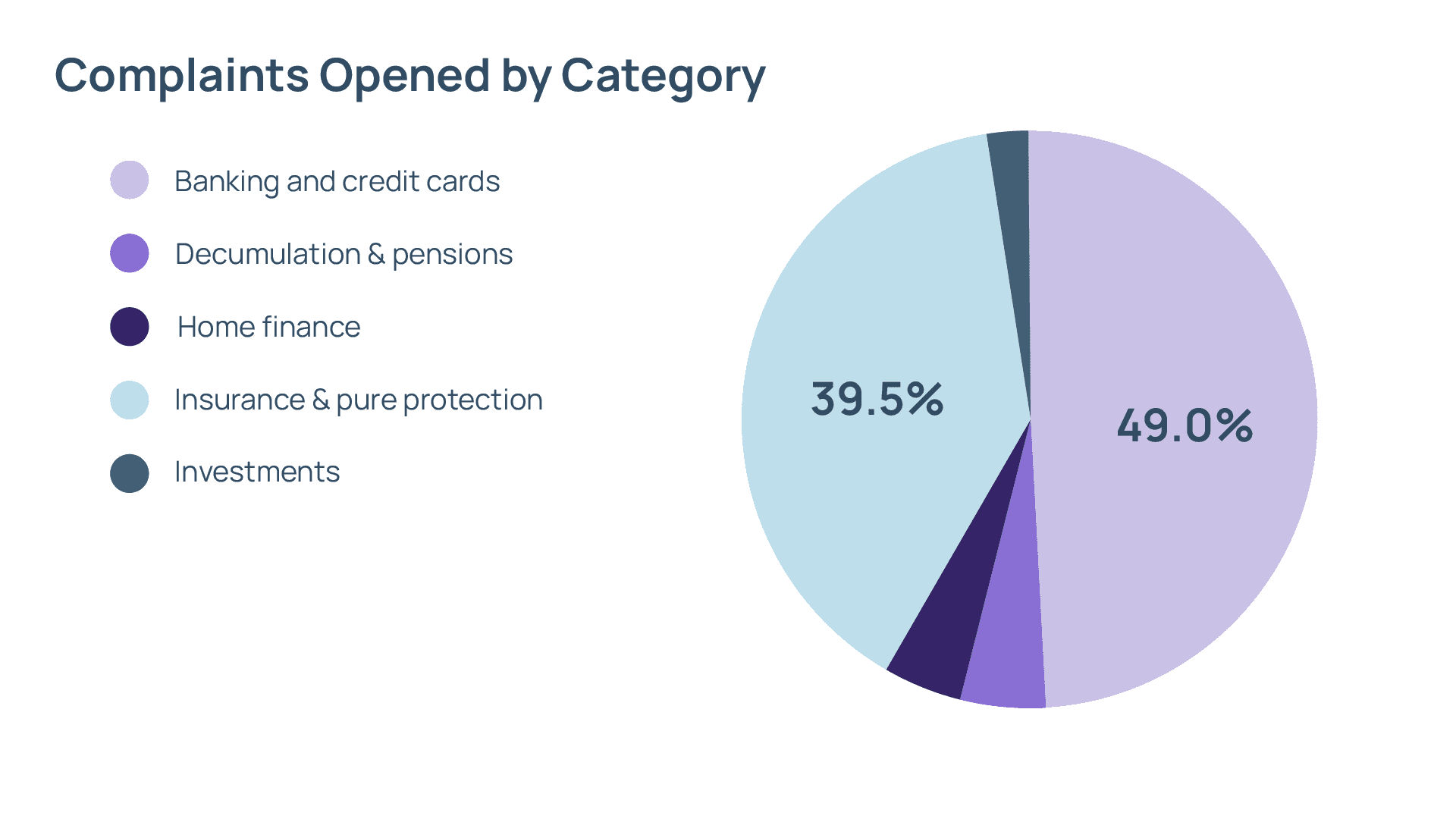

Here's what the numbers tell us: This data comes from 220 companies, including 52 banks, over six months in 2024. And the results are eye-opening. Nearly half (49%) of all complaints are about cards and payments. Add in insurance complaints (40%), and you've got 89% of all customer problems. That's a huge chunk of unhappy customers dealing with payment issues

The Rising Cost of a Stagnant Process

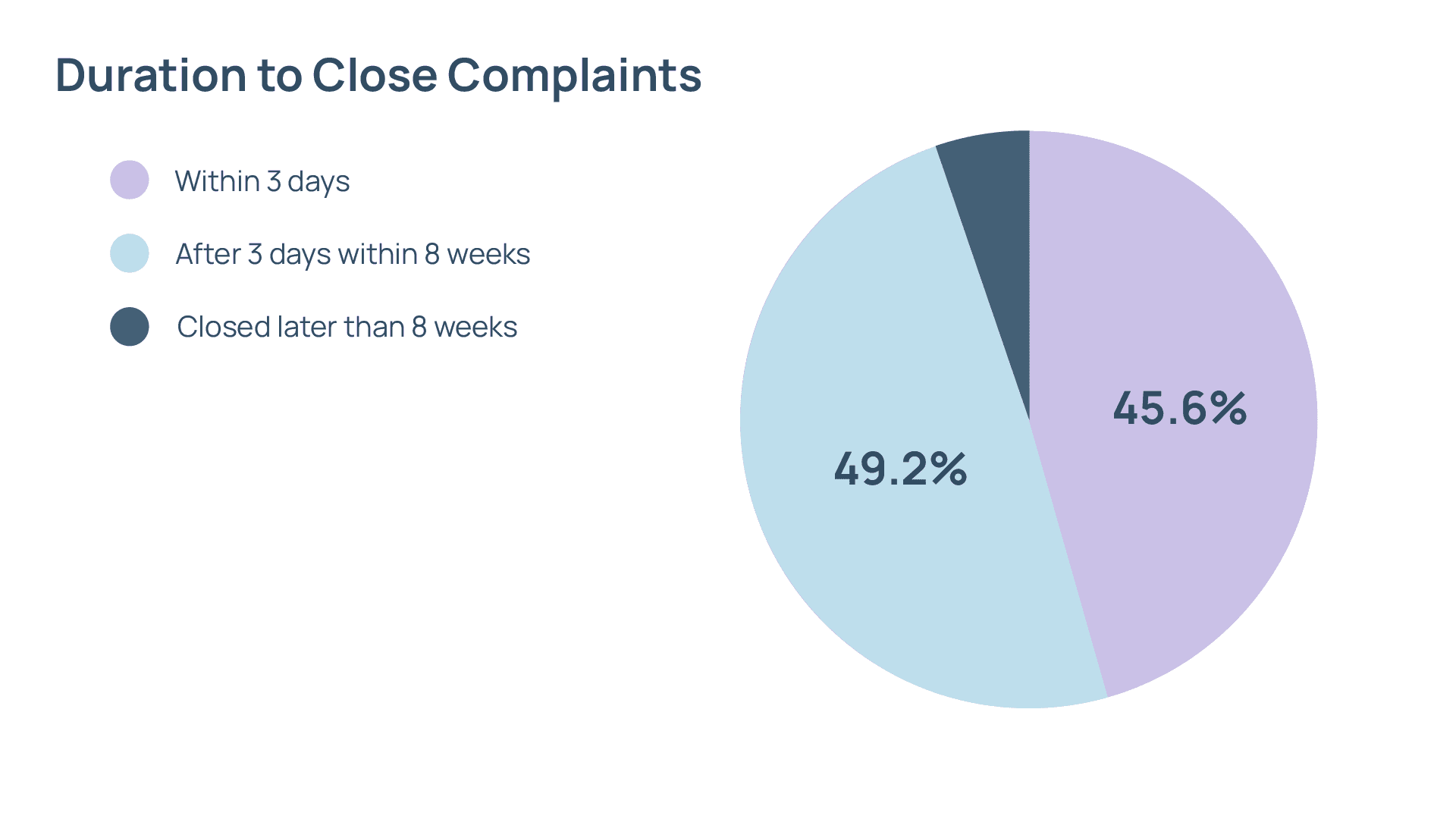

The FCA data reveals a troubling reality about dispute resolution efficiency across the industry. Here's the problem: Only 46% of complaints get sorted within three days. That means more than half take longer. And it's getting worse. A small percentage of total complaints are being resolved quickly now compared to 2022-2024, suggesting that complexity and workload are outpacing operational improvements

Even more concerning? Nearly half (49%) of complaints take weeks to resolve. Think about that. You have a problem with your card, and there's almost a 50/50 chance you'll be waiting weeks for an answer.

This costs banks serious money. Every complaint sitting in the system for weeks means staff time, paperwork, and frustrated customers. When half your complaints take weeks to solve, you're basically running a slow, expensive process that nobody likes

The Erosion of Trust: From a Card Dispute to a Lost Customer

Beyond the operational costs, the most significant long-term risk exposed by this data is the erosion of customer trust. The number of complaints that are ultimately upheld in a customer’s favour is a powerful metric. When a Financial Institution admits that a complaint is valid, it’s an acknowledgement of a failure in its processes, products, or services.

And here's the kicker: 56% of complaints are upheld. And around half of them (the 49% mentioned above) had to wait for more than 3 days for a resolution. That means more than half the time, the customer was right. Think about what that means. Most people complaining aren't just being difficult. They have legitimate problems that the bank should have fixed from the start.

The upheld rates for some of the UK’s largest banks are substantial. Banks like HSBC, Lloyds, Santander, and Barclays all had tens of thousands of complaints upheld in just one six-month period. This indicates that many customer grievances are not frivolous but are justified issues that should have been addressed from the outset.

A negative experience in a core service like card payments can have a ripple effect across a customer's entire relationship with a bank. A stressful or inefficient fraud resolution process can damage a customer's confidence in a bank’s reliability, potentially influencing their decision to look elsewhere for higher-value products such as a loan or a mortgage. In a competitive market, the ability to handle complaints effectively is not just a measure of its customer service, but a leading indicator of its overall business health.

The trend isn't improving either. Complaint numbers are staying the same or going up. So we're looking at more complaints, longer wait times, and most customers being proven right. That's not a recipe for happy customers

Moving Forward: A Proactive Approach to Complaints

The takeaway is clear: complaints data should not be viewed as a backward-looking compliance exercise. It is a strategic tool for proactive business improvement. By leveraging technology to automate the triage of simple cases, banks can free up human agents to provide a more empathetic and effective service for complex issues. Adopting this strategic approach can transform a bank’s complaints framework from a costly liability into a powerful engine for building and protecting customer trust.