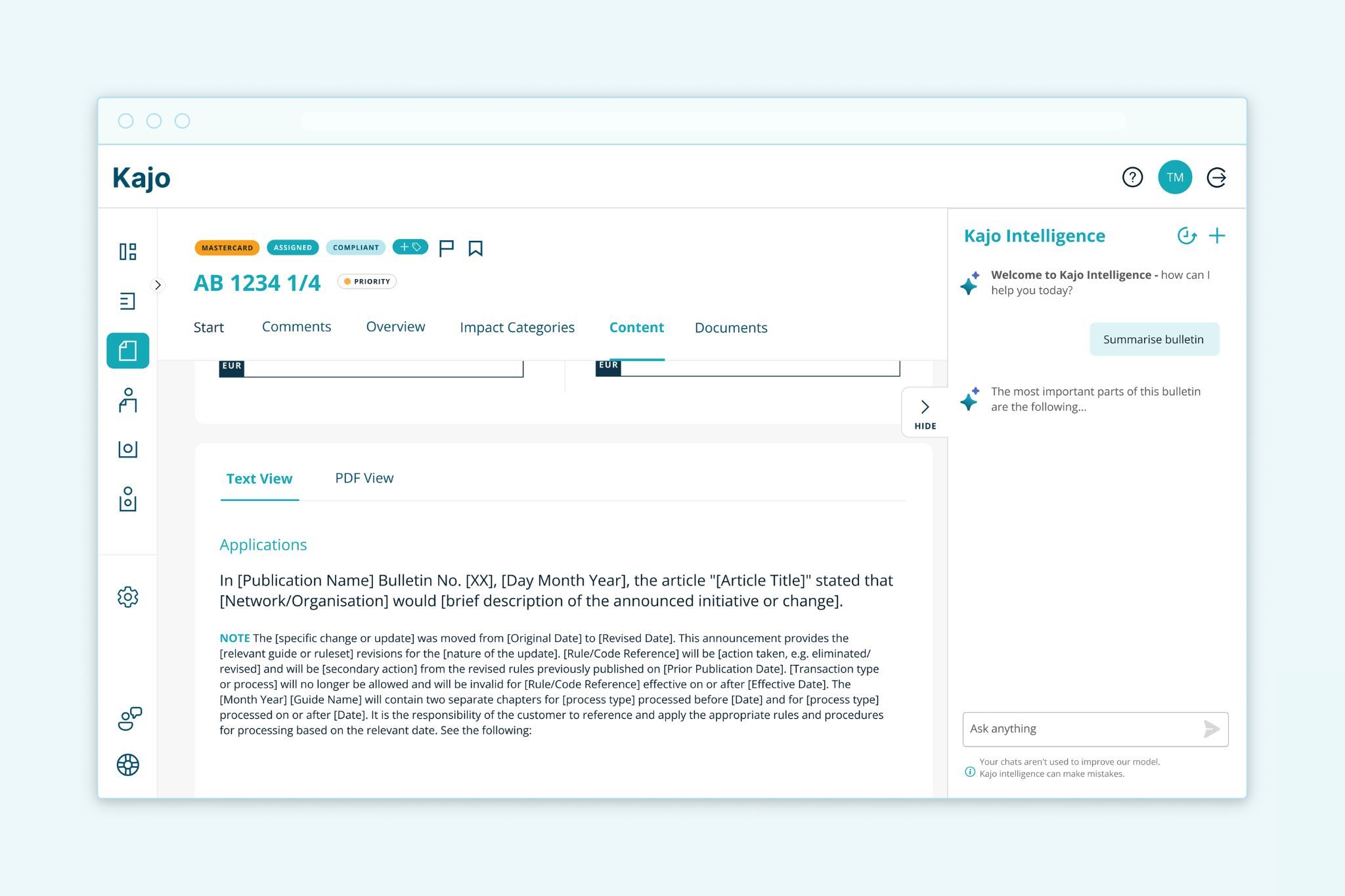

→ AI-driven bulletin analysis

The hardest part of compliance is interpreting bulletins. Legal language, cross-references to prior mandates, and ambiguous applicability all require expert judgement that scales poorly. AI is now doing the first pass: summarising bulletins, identifying affected products and systems, scoring relevance against the issuer's specific licence and footprint, and drafting impact assessments. Compliance teams move from manual interpretation to reviewing and approving machine-generated analysis.

→ Product roadmap intelligence

Every issuer treats scheme compliance as something to do after the bulletins arrive. The unrecognised opportunity is what those bulletins represent: every mandate payment network publishes is a signal of where the entire payments industry is heading, six to twenty-four months before the change is visible in the market. The issuers that win the next cycle will be the ones that read scheme bulletins as product roadmap intelligence. New authentication standards, tokenisation rules, interchange category creations – read early, they become first-to-market product features.

→ Compliance as proactive planning

Manual compliance is reactive by design. The shift underway is to treat compliance as a planning function: known mandates surfaced months ahead, deadlines synced to the product and engineering roadmap, and resource allocation decided before the deadline pressure starts. Done well, this collapses the volume of "emergency" implementations and frees the team to influence rather than absorb scheme changes.

→ Audit-readiness by default

Regulators and scheme auditors increasingly expect issuers to demonstrate not just compliance, but the full evidentiary chain: how the requirement was identified, when, by whom, and what action was taken. Manual processes produce audit trails after the fact, reconstructed from emails and spreadsheets. It's a process that takes weeks and rarely holds up cleanly. Modern compliance systems generate the audit trail as a by-product of the workflow itself: every bulletin received, every decision made, every task closed is timestamped and attributable.