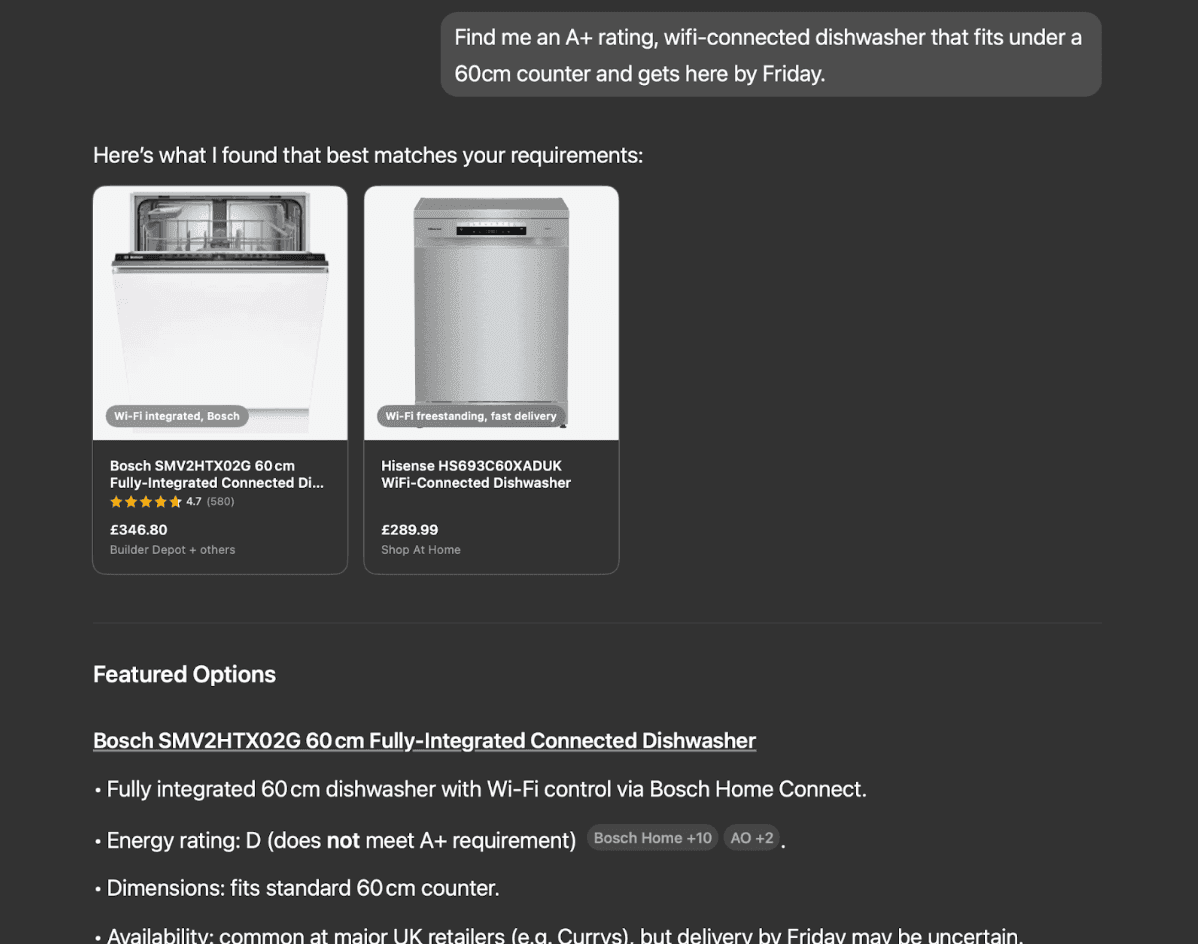

It starts with a simple request: "Find me an A+ rating, wifi-connected dishwasher that fits under a 60cm counter and gets here by Friday."

I didn’t search. I didn't scroll. I didn't compare reviews, open tabs, or get sucked into decision fatigue. My AI agent did it for me. It knew my budget, my past purchases, and my goals. It filtered the noise. Ten minutes later, I had a shortlist. Five minutes after that, the order was in, complete with cashback applied and delivery scheduled. Zero friction. No abandoned cart. No marketing funnel. It hit me: this wasn’t shopping. This was solving a problem. And not once did I visit a merchant's site. Not once did I interact with a payment provider.

So… where does that leave everyone else?

We're entering a new age, one where AI agents act on behalf of consumers. These agents don't get tired. They don't browse aimlessly. They don't fall for banner ads. They don't care about your carefully crafted brand voice. They are data-driven and care about parameters. They scan, compare, and transact across APIs and marketplaces. And they're doing it faster, smarter, and with more context than any human shopper ever could. And here's the kicker: most businesses are utterly unprepared.

We unpacked these shifts and what they mean for fraud, payments, and disputes in our latest webinar. Watch it here.

The old playbook no longer works

The digital strategies we've perfected over the past two decades like SEO, email journeys, loyalty programmes, and checkout optimisations, were built with human psychology in mind. But your next customer isn't human. It's algorithmic. That means:

- Brand loyalty is out. Utility is in.

- Emotional storytelling takes a backseat to structure and metadata

- SEO becomes ASO (Agentic Search Optimisation) or GEO (Generative Engine Optimisation)

- Payment forms become invisible as agents can execute direct API calls

- Your best fraud model? It may now block your actual buyers

So here's the uncomfortable truth: If your business is designed for people, you're about to be disrupted by machines acting for people.

The fight for relevance

For merchants, this is both terrifying and liberating. Terrifying, because the rules of engagement are shifting under your feet. Liberating, because for the first time in years, you can truly take back control. No more renting audiences from platforms.

No more losing margin to middlemen.

You can now build direct relationships not with people, but with the agents they trust.

But only if you adapt.

What about payments?

Let's talk about the elephant in the (server) room. Payment infrastructure is built for humans. Click-to-Pay. CAPTCHA. Card verification. Consent screens. AI agents don't do clicks. They transact directly. And most of our infrastructure, especially fraud models, can't tell the difference between a rogue bot and a legitimate shopping agent.

Issuers, PSPs, acquirers, you’re at risk of becoming invisible. If agents don't see you, you're not in the flow. And if you're not in the flow, you're not getting transactions.

And then there’s the law

Who’s responsible if an agent overspends? How do you tax an order placed by a server in a different country? Can merchants block AI agents without violating consumer rights? The truth: our legal frameworks are built for humans. They don’t yet know what to do with Custobots. And that’s a huge risk but also a huge opportunity for those ready to shape the next regulatory frontier.

Are we ready for a world where the buyer isn't human?

I think we are getting there faster than we think. But there is still a lot of uncertainty how exactly agentic commerce will develop. Here are my top considerations for merchants, issuers and payment service providers.

For Merchants, this means:

- You're no longer selling to emotions. You're selling to logic. Agents evaluate specs, price, reviews, and availability. If your data isn't complete, accurate, and structured you won't even make the shortlist.

- First-party data is gold. The better you know your customer, the better you can serve their agent. And the more leverage you have to escape the grip of aggregators and ad platforms.

- Product experience trumps brand loyalty. A Custobot doesn't care about your TV campaign but it will remember if your delivery was late, your sustainability claims were verified, or your returns process was smooth.

- You need to decide: Will you allow AI agents on your site? Will you build APIs for them? Or will you block them, and risk irrelevance?

Agentic commerce could empower merchants to rebuild direct, performant relationships if they're bold enough to shift their strategy from storytelling to service.

For Issuers and Payment Providers, the ground is shifting even more.

- You're being cut out of the checkout. AI agents don't fill in forms. They can make direct API calls often skipping the embedded payment UIs entirely. If you're not present at the point of decision, you're not part of the transaction.

- Fraud models must evolve. Today's systems look for "bot-like behaviour" and flag it as a risk. But tomorrow's legitimate customer will be a bot. So false positives will most-likely skyrocket, sales drop, and consumer trust erode.

- You"ll need to support agent-specific features, such as tokenised wallets with spending rules, usage timeframes, and merchant-type restrictions. Without this, AI agents may simply route transactions through someone else's infrastructure.

- Identity becomes core. Know Your Agent (KYA) may become just as critical as KYC. Issuers who invest in verifying digital agents, securing consent layers, and offering intelligent controls will have a competitive edge.

- Profit pools are at risk. If the new gatekeepers of commerce are AI platforms, rather than search engines or commerce platforms, then traditional players may find themselves disintermediated, reduced to utilities rather than relationship owners.

So, for issuers, the real questions is: "how do we become indispensable in this new flow?"

Are you prepared to rebuild your customer journey, not for clicks, but for code? And most importantly, will you fight to stay in the flow, or let someone else own the rails of tomorrow's commerce?