When a cardholder challenges a transaction, whether they claim it's fraud, a billing mistake, or a purchase issue, their claim enters a dispute lifecycle.

This is the step-by-step process payment networks like Visa and Mastercard use to decide who's financially responsible and how to resolve the matter.

The details can get technical, but at its core, the lifecycle is about correcting errors fairly and quickly. Understanding how it works helps issuers, acquirers, and even merchants handle cases efficiently, avoid rule violations, and reduce costs.

The stages of the dispute lifecycle

While Visa and Mastercard use different terminology and have slightly different rules, the flow is remarkably similar.

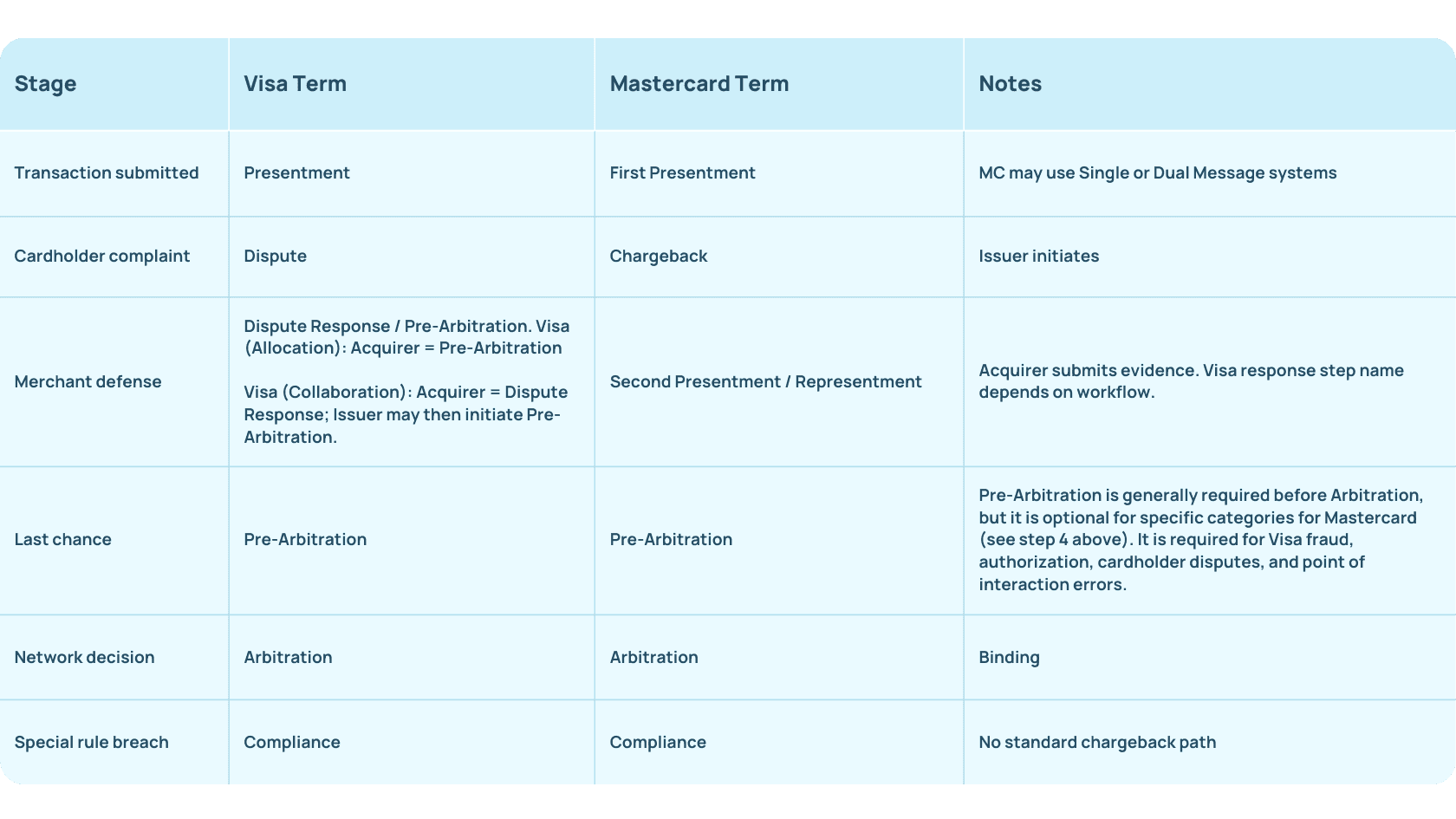

1. Presentment

This is when the merchant's bank (the Acquirer) sends the transaction through the network for processing. The network routes it to the issuer, who posts it to the cardholder's account.

Visa & Mastercard: Funds move between acquirer and issuer through clearing and settlement.

Mastercard twist:

- Dual Message System (DMS) - Authorisation and settlement are separate messages.

- Single Message System (SMS) - Authorisation, clearing, and settlement all happen in one step.

Visa spin:

- VisaNet Integrated Payment (VIP) - The online component of VisaNet that provides routing and processing of Authorisations and financial Transactions

- BASE II - A file-based VisaNet service comprised of functions to collect, clear, settle, and deliver files of financial and non-financial activity between Visa and Members.

2. Pre-dispute

Before a formal dispute is even filed, there's often a pre-dispute stage.

Here’s what it looks like:

- A cardholder sees something odd on their account (a charge they don't recognise, goods they never received, or a duplicate)

- They contact their issuer

- The issuer may use network pre-dispute tools to check with the merchant or acquirer before escalating

Visa: Rapid Dispute Resolution (RDR) Mastercard: Collaboration tools / Ethoca Alerts

At this stage, merchants can choose to refund automatically rather than fight, avoiding a formal dispute altogether.

Why pre-dispute matters?

- Issuers: Save time and cost by resolving early

- Acquirers & merchants: Prevent disputes from hitting ratios that could trigger monitoring programs.

- Cardholders: Get a quicker resolution.

3. Dispute (Visa) / Chargeback (Mastercard)

If a cardholder spots a problem, they contact their issuer. The issuer:

- Reviews the claim

- Verifies it meets network rules

- Gathers supporting documentation

- Sends the dispute/chargeback to the acquirer

If valid, the disputed amount is temporarily refunded to the cardholder and debited from the acquirer. Just a note here, the payment networks move funds between issuer/acquirer via dispute financials; provisional credit to the cardholder is handled by the issuer and may be required by regulation or internal policy, but it's not the network directly refunding the cardholder

- Visa: The term is "Dispute."

- Mastercard: The term is "Chargeback" and issuers are allowed only one chargeback per transaction amount, though it can be total or partial. So in other words the issuer can submit a chargeback for the full or a partial amount, and may submit multiple partial chargebacks so long as the combined total does not exceed the original transaction amount

4. Dispute response (Visa) / Second presentment or Representment (Mastercard)

This is the acquirer's chance to fight back if they believe the dispute isn't valid.

They may:

- Provide missing documents

- Show proof of cardholder authorisation

- Prove the goods or services were delivered as described

These are just a few examples of valid reasons.

Visa:

- "Pre-arbitration" for Fraud/Authorisation disputes

- "Dispute response" for Processing errors/Consumer disputes

Mastercard: Calls this step "Second presentment" or "Representment."

5. Pre-arbitration

This is essentially the last chance for issuers and acquirers to resolve the dispute before the network gets involved.

Visa:

- Pre-arbitration precedes Arbitration in both workflows. In Allocation (Fraud/Authorisation), the acquirer initiates Pre-arbitration; in Collaboration (Consumer/Processing error), the issuer initiates Pre-arbitration after receiving the acquirer's Dispute response.

- Used to either accept or reject evidence from the other side.

Mastercard:

- Pre-arbitration is generally required before Arbitration, but it is optional for specific categories (e.g., ATM, authorisation-related in Dual Message System). Pre-arbitration cases are filed by the issuer; the acquirer may accept, reject, or take no action.

6. Arbitration

If neither side agrees, Visa or Mastercard steps in.

The network reviews all documentation, applies its rules, and issues a final, binding decision.

Visa: Pre-arbitration must happen first.

Mastercard: Pre-arbitration is optional.

Compliance

If no standard chargeback rule covers the situation, but a network rule violation has caused financial loss, a compliance case can be filed. To clarify, this is not a 7th step, as it doesn't require the previous steps to have happened but is a completely independent flow from pre-compliance to compliance.

- Used for edge cases where normal dispute rights don’t apply.

- Can be initiated by either issuer or acquirer.

Why the lifecycle differs by dispute type

Not all disputes are created equal.

For example:

- Fraud and Authorisation disputes often involve clear liability shifts, like when a merchant didn't use EMV chip technology.

- Processing errors and Consumer disputes tend to be more complex, requiring detailed evidence and back-and-forth between issuer and acquirer.

Networks design separate flows for these types so they can resolve simpler cases quickly and dedicate more time to the complicated ones.

This is important for both Issuers and Acquirers

- Issuers need to know the steps to meet strict network deadlines and protect cardholder trust.

- Acquirers need to understand when and how to respond to keep merchants’ dispute ratios under control.

Both sides benefit from fewer escalations, which save time and fees.

Visa vs. Mastercard lifecycle at a glance

The dispute lifecycle is more than a bureaucratic sequence. It's a framework for deciding who's responsible, how fast the cardholder is refunded, and whether the merchant takes the loss. When issuers and acquirers understand each step and adapt their processes accordingly, they resolve cases faster, save money, and improve customer satisfaction.

Want to resolve disputes faster? Manage every stage, from fraud reporting and pre-dispute to arbitration, all in one place.