In the modern payments landscape, speed is the ultimate currency. While real-time payments have become the norm, the back-office processes for managing fraud, errors, and disputes have historically lagged behind. This operational gap is driven by siloed data, manual workflows, and fragmented communication channels.

Regulatory frameworks like the EU's PSD2, the UK's PSRs 2017, and the US's Regulation E and Z were designed to close this gap by mandating strict timelines for cardholder refunds. However, for many card issuers, these rules are viewed as a high-pressure compliance hurdle rather than an opportunity.

By rethinking how to handle these mandates, issuers can transform regulatory obligation into a distinct operational advantage and a superior customer experience.

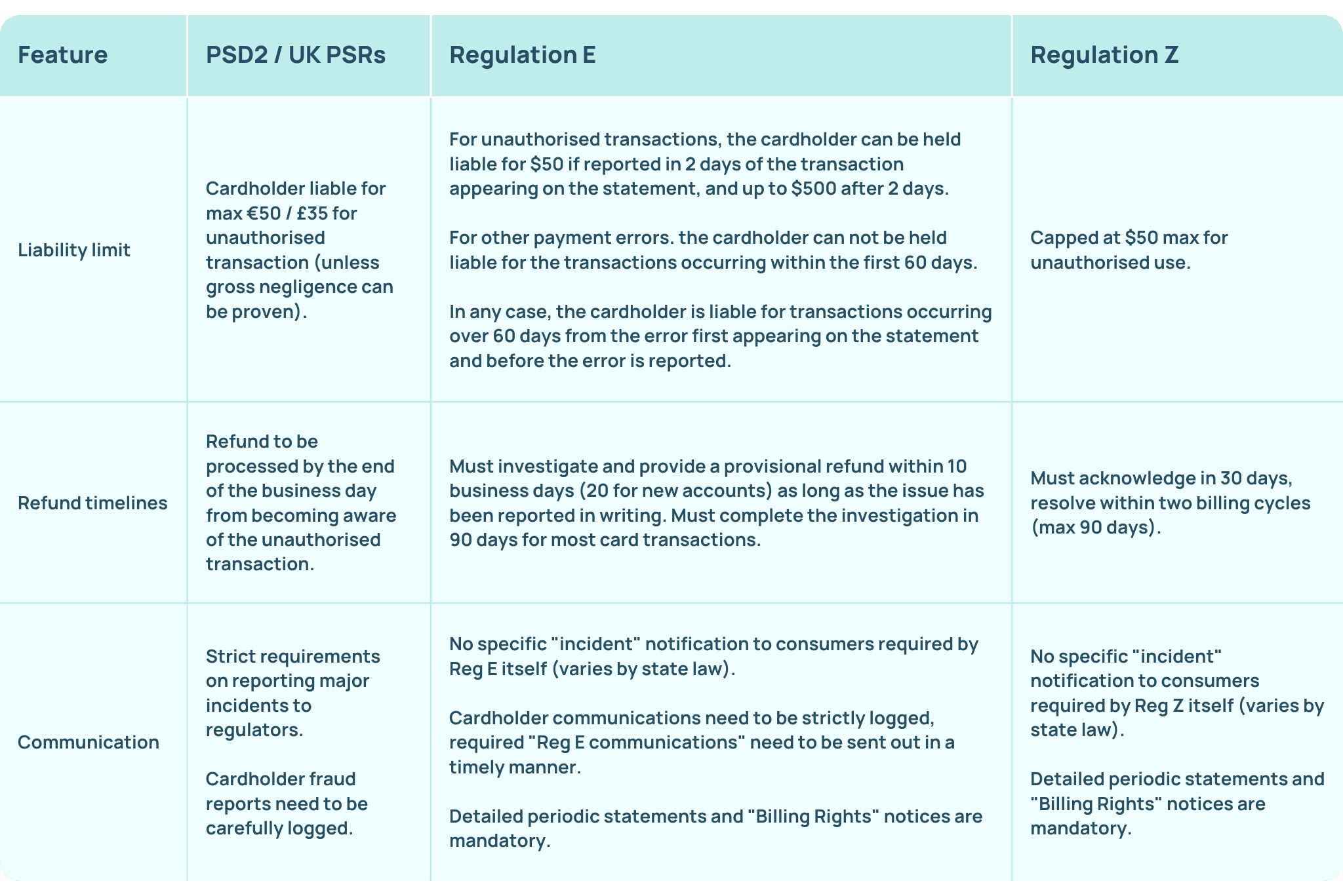

Comparing the regulatory mandates

While consumer protection remains a universal objective, procedural requirements and their operational impacts on issuers vary significantly across regions:

- EU (PSD2) & UK (PSRs 2017): For unauthorised transactions, issuers must provide a refund by the end of the next business day after being notified. The only way to bypass this "Day+1" rule is if the issuer has reasonable grounds to suspect fraud and communicates these grounds in writing to the national authority.

- US Debit Cards (Reg E): If an investigation into a "payment error" can't be completed within 10 business days (for new accounts – 20 days), and the cardholder has reported the issue in writing, the issuer must provide a provisional credit. The investigation can then be extended to 90 days (or in case of domestic ATM transactions, only 45 days), but you must strictly track and send written notices for every step.

- US Credit Cards (Reg Z): Cardholders have the right to withhold payment for disputed amounts while the issuer follows a strict 30-day acknowledgement and 90-day resolution window (or two complete billing cycles). Missing a single letter or sending it late constitutes a compliance breach, even if the final outcome was correct.

Why issuers struggle: the manual processing bottleneck

Issuers traditionally handle these requirements through scaling up their front-office and chargeback teams. However, this creates a heavy operational burden, as explored in our deep dive on the cost of time. Manual processes simply can’t keep pace with strict PSD2 or other regulatory timelines.

Three factors are making this model unsustainable:

- The refund-first dilemma. In the EU and UK, the one-day window is so tight that issuers often feel forced to refund immediately to stay compliant, even if they suspect "friendly fraud" (first-party misuse). Without robust automation, there is often no time to distinguish legitimate fraud from cardholder misuse.

- The communication trap. In the US, missing a single written notice, whether it’s the acknowledgement letter, provisional credit notice, or final determination, constitutes a compliance breach. Managing these across thousands of cases via legacy systems is inherently error-prone.

- Volume spikes. BIN attacks or seasonal shopping surges can stall a manual team, leading to missed deadlines and regulatory fines.

How Amiko automates dispute excellence

Rivero's Amiko platform provides tracking options for regulatory obligation as part of the general dispute management tooling, integrating the separate processes into a single flow.

→ Automated timeline tracking

Amiko separates regulatory timeframes (the time you have to refund the customer under PSD2, Reg E, or Reg Z) from general operational scheme SLAs (the time you have to file a chargeback with Visa/Mastercard), which prevents the common error of meeting a scheme deadline but failing a legal mandate. The system automatically calculates due dates for refunds and notifications based on the specific regulation, ensuring no deadline is ever missed due to human error.

→ Triage at intake with the 24/7 Virtual Agent

To tackle volume volatility and solve the "refund-first" risk, Amiko utilises a Virtual Agent (chatbot) for digital intake. Amiko's Virtual Agent integrates directly into the bank’s mobile app or portal.

The virtual agent validates and triages customer claims in real-time, resolving inquiries before they become cases.

- It uses transaction data to ask the right questions at the point of entry.

- It helps cardholders recognise transactions (for example, by showing a recognisable merchant’s name, transaction location, etc.) and therefore deflect friendly /first-party fraud (~80% of fraud claims).

- It educates cardholders (e.g., explaining whether there is a right to a chargeback or whether they should refer to merchants first), resulting in ~20% zero-touch resolution.

- For valid claims, the case is already pre-validated, pre-filled with chargeback reason codes, and contains all relevant documentation.

- When enabled, the issuer can automate sending cases to merchant collaboration platforms (e.g., Ethoca) and define a regulatory-compliant timeframe.

- If the merchant refunds the cardholder within that window, the case is automatically resolved (~35% zero-touch recovery).

→ Straight-through cardholder account adjustment

Amiko can integrate with an issuer's systems to trigger cardholder account adjustments, provisional credits, and write-off bookings. This reduces the need for agents to switch to another system and, when set to automated, minimises the need for manual procedures.

→ Intelligent automation for volume management

When a large-scale fraud event occurs, the specialist can use Bulk Actions to apply decisions or submit chargebacks across hundreds of transactions at once. This ensures that a single large fraud case no longer has a considerable impact on the general backlog.

Amiko also provides automations for chargeback processing under issuer-defined rules and thresholds, along with pre-disputes and refunds.

→ Streamlined communications

The platform automatically handles the generation and delivery of cardholder communication and mandatory compliance letters:

- Instant acknowledgements: automated confirmations are sent immediately upon receipt of the claims

- Provisional credit notices: triggered automatically the moment credit is booked to the accounts

- Final determinations: generated as a native step of the case closure process

Amiko also supports PSD2 compliance tracking for fraud claims, helping teams monitor investigation deadlines at case level and clearly record whether a claim is compliant, delayed, or not applicable. With automation in progress to connect booking actions and compliance status, issuers gain tighter operational control over PSD2 obligations and a more scalable way to manage time-sensitive fraud workflows.

Disputes as a strategic lever

Regulatory pressure is not easing. PSD2 and Regulation E/Z continue to raise the bar as global scrutiny keeps growing. The true transformation lies in moving beyond reactive compliance and adopting a unified automated dispute management strategy.

When dispute management workflow is automated, the benefits ripple across the entire organisation:

- Operational savings: by automating routine tasks (cardholder account adjustments, zero-touch resolution & recovery, bulk actions for high-volume processing), issuers reduce the cost-per-dispute.

- Reduced write-offs: better triage, resolution and deflection at intake means fewer unjustified cases and refunds.

- Customer trust: a customer who receives quick, friendly treatment is more likely to keep your card "top-of-wallet".

With the right infrastructure in place, it becomes a world-class card operation. That is how compliance transforms from a defensive obligation into a true competitive edge.

If you would like to explore how this works in practice, we are happy to walk you through a personalised demo.