Every time a cardholder taps, swipes, or enters their card details online, a complex redistribution of value takes place behind the scenes. Understanding how money flows through the four-party card payment ecosystem is essential for anyone working in payments, whether you are on the issuing side, the acquiring side, or anywhere in between.

This article breaks down the revenue models of each participant in the four-party scheme and explains the economic forces that keep the ecosystem running.

To build a sustainable card program, one must look beyond simple transaction volumes. Understanding the economic interplay between the merchant, the acquirer, the network, and the issuer is the first step toward protecting your margins.

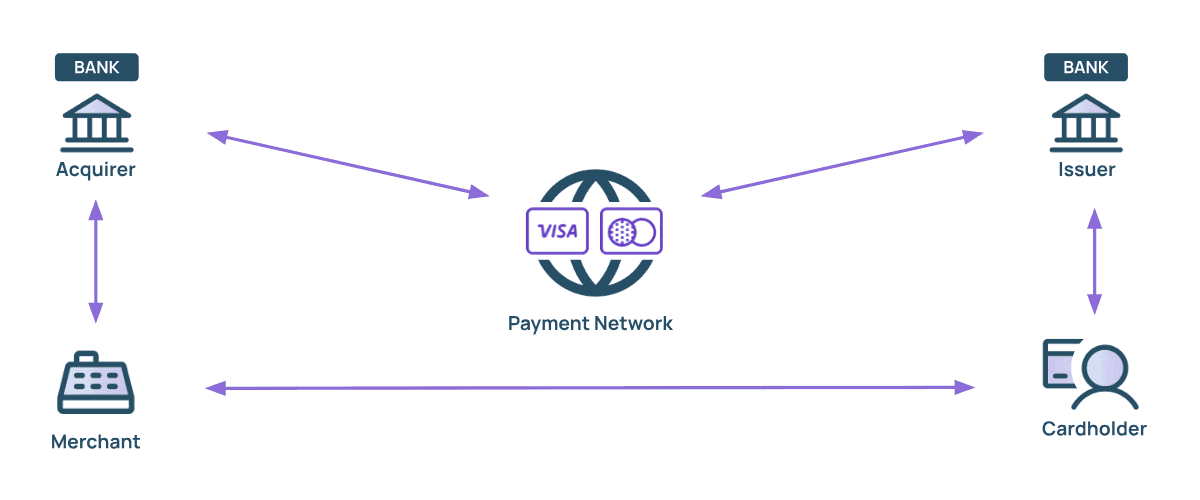

The four parties & the network that connects them

The four-party card scheme model consists of four core participants: the cardholder, the issuer (the cardholder's bank), the acquirer (the merchant's bank or payment processor), and the merchant. Connecting all of them is the payment network (scheme) operated by organisations such as Visa and Mastercard.

The key idea: every card transaction distributes revenue across multiple participants through interchange fees, scheme fees, and merchant service charges.

For a closer look at how each of these parties interacts operationally, from card issuance to authorisation and clearing, see our deep dive into the card payments value chain.

How the value gets distributed

It is a fundamental truth of the payments world: the merchant funds the entire ecosystem. When a cardholder spends $100, the merchant does not receive $100. Instead, they receive the net amount after the Merchant Service Charge (MSC) has been deducted by their acquirer, typically between 1% and 3% of the transaction value.

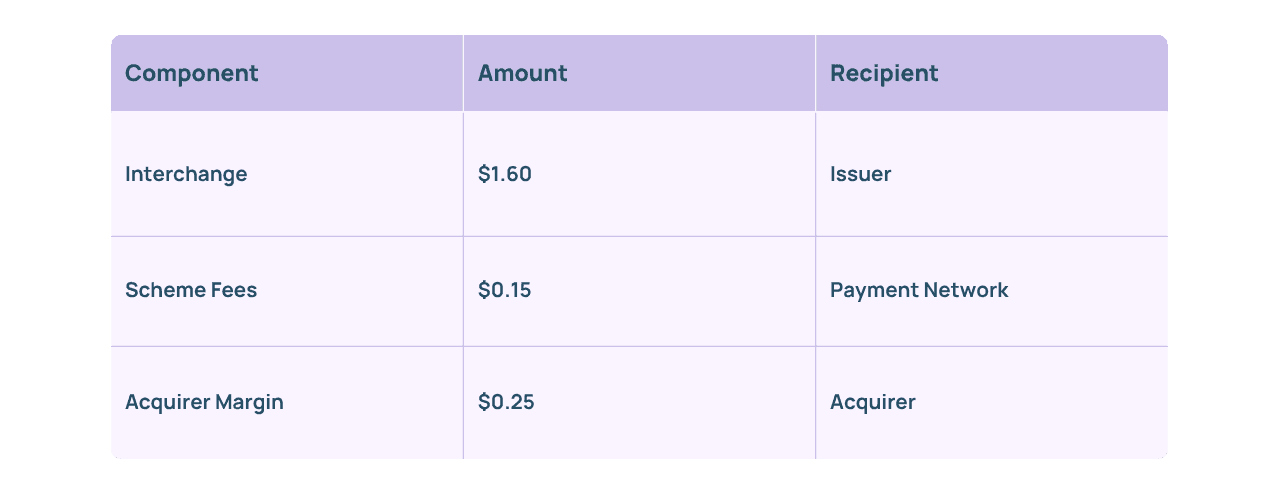

This MSC is the primary fuel for the four parties. For a hypothetical $100 purchase with a $2.00 MSC, the redistribution typically looks as follows:

- Interchange fees: The portion passed to the issuer as an incentive to issue cards and fund rewards (e.g., $1.60).

- Scheme fees: The portion collected by the payment network for providing the infrastructure (e.g., $0.15).

- Acquirer margin: The portion retained by the merchant’s bank (e.g., $0.25).

Issuer revenue

Issuers, typically the cardholder's bank, have the most diversified revenue model in the ecosystem. Their earnings rest on four pillars.

1. Interchange fees. Interchange is the most consistent revenue stream for issuers. It is paid by the acquirer to the issuer on every transaction and serves as a financial incentive for banks to issue cards. Interchange fees typically range from 0.2% to 2.5% and depend on several parameters: the card type (with the "Honor All Cards" rule requiring merchants to accept premium cards alongside standard ones), the merchant category code (MCC), the point-of-sale entry mode (chip-and-PIN vs. e-commerce), the transaction location (domestic vs. cross-border), and data quality (particularly relevant for B2B transactions where richer data reduces fraud risk).

In Europe, the Interchange Fee Regulation (IFR) caps consumer interchange at 0.2% for debit and 0.3% for credit. These caps were determined through the Merchant Indifference Test, a strategic assessment designed to identify the threshold at which merchants were indifferent between accepting a card payment and handling cash. Outside Europe, particularly in the US and certain emerging markets, interchange rates can be significantly higher.

2. Interest income. While interchange is the most stable revenue line, interest income from credit cards is usually the largest revenue driver for issuers. When cardholders carry revolving balances rather than paying off their statements in full, the accumulated interest represents substantial earnings. This also explains why dedicated consumer charge card products, which require full monthly repayment and generate no interest income, are relatively rare.

3. Cardholder fees. Issuers also earn from a range of fees charged directly to the cardholder: annual card fees, foreign exchange markups on cross-currency transactions, late payment fees, and cash advance fees for ATM withdrawals.

4. Network incentives. Finally, issuers can receive rebates or incentives from Visa and Mastercard based on transaction volume. These are negotiated directly in contracts with the payment schemes (for example, committing to process a certain volume of transactions annually through a particular network in exchange for a partial refund).

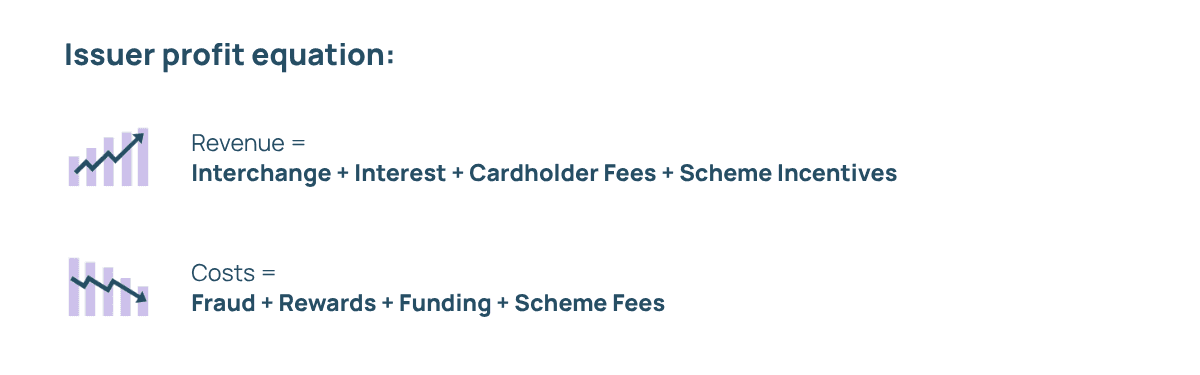

The issuer profit equation brings this together. Revenue equals interchange plus interest plus cardholder fees plus scheme incentives, minus costs including fraud losses, cardholder rewards payouts, funding costs (the bank's cost to borrow the money it lends on credit), and scheme fees.

Fraud is a major cost that can quickly eat into thin margins, which makes efficient recovery critical. When revenue is capped, as it is in Europe, protecting what remains means cutting losses and inefficiencies rather than chasing new income. That is where dispute handling becomes a profit lever: advanced tools like Amiko automate recovery and dispute handling, turning a cost center into a streamlined system that protects revenue.

Acquirer revenue

The acquirer's primary revenue source is the Merchant Service Charge (MSC), which is structured as:

MSC = Interchange + Scheme Fees + Acquirer Margin

The acquirer keeps only the margin component, which typically sits in the range of 10-40 basis points of the transaction value. A basis point is one hundredth of a percentage point, so 10 basis points equals 0.1%.

Because processing margins are under constant downward pressure, acquirers increasingly look to additional revenue streams that often carry higher margins than basic transaction processing. These include:

- payment gateways (secure channel for data from merchant to acquirer/network);

- fraud and dispute prevention tools (a major pain point for merchants);

- tokenisation services (to enable merchants to replace stored card numbers with network tokens);

- POS terminal sales or rentals;

- cross-border payment services with multi-currency pricing and/or settlement;

- data analytics offerings (total sales volume, average transaction value, payment method breakdown, refund and decline rates).

Some acquirers have also begun offering guaranteed payment services, effectively taking on the fraud risk themselves. If a transaction turns out to be fraudulent, the acquirer absorbs the loss rather than passing it to the merchant, relying on their own fraud prevention tools to make this insurance model profitable.

Card network revenue

Payment networks earn primarily through scheme fees charged to issuers and acquirers.

But these are not one or two line items on an invoice, network fee catalogues include hundreds of individual fees. Some are charged per transaction, some as a percentage of transaction value, some at the programme level, some as monthly subscriptions for optional services, and some as one-time penalties for compliance breaches.

The main categories of scheme fees include:

- processing fees (covering the routing of authorisation messages, decline handling, transaction processing events);

- assessment fees (a percentage of transaction volume reflecting general network usage, infrastructure, and network participation costs);

- cross-border fees (triggered when the issuer and merchant are in different countries);

- digital enablement and tokenisation fees (covering e-commerce infrastructure and digital wallet services like Apple Pay and Google Pay);

- security and compliance fees (covering fraud monitoring, chargeback-related charges, 3D Secure fees, and penalties for non-compliance with network rules).

Altogether, these fees typically range from 10 to 50 basis points (0.10%-0.50% of transaction value).

Merchant economics

Merchants are the paying participants in the ecosystem. Their costs include the merchant service charge, terminal and gateway fees, fraud losses, and chargebacks, typically totalling 1-3% of transaction value.

So why do merchants accept cards at all? Because card acceptance enables higher sales conversion, e-commerce capability, larger average transaction values, reduced cash handling costs.

Accepting cards is fundamentally a cost of doing business in the modern economy.

Cardholder economics

Cardholders typically do not pay per transaction. Their costs come in the form of annual card fees, interest on revolving credit card balances, foreign exchange markups, and late payment fees.

In return, cardholders receive: payment convenience and, particularly with credit cards, rewards and benefits such as cashback, airline miles, loyalty points, purchase protection, and travel benefits.

These rewards are funded primarily by interchange revenue. Because European interchange is capped at relatively low levels, reward programmes in Europe tend to be less generous than those available in markets like the United States.

Bringing it all together

The payment model is a carefully balanced redistribution mechanism. The merchant funds the transaction ecosystem. The issuer earns from interchange and interest. The acquirer earns on the merchant service margin. The network earns from scheme fees. And the cardholder receives the convenience of cashless payment along with potential rewards.

Interchange transfers value from merchants to issuers, while scheme fees extract revenue from both issuers and acquirers. Understanding all these flows and the pressures acting on each party is foundational for anyone making strategic decisions in the payments industry.